Tax Implications For Entrepreneurs, Consultants, Stackers, and Other Pirates

Most people plan their tax preparation around the premise that they have one job or one source of income - what if you don't?

Watch my daddy in bed a-dyin’

Watched his hair been turnin’ grey, yeah

He’s been workin’ and slavin’ his life away

I know he’s been workin’ so hard

We gotta get out of this place

If it’s the last thing we ever do

We gotta get out of this place

‘Cause girl, there’s a better life for me and you

- We Gotta Get Out Of This Place, The Animals

It was only a few minutes after my last article on taxes before people started asking me what to for situations where they had multiple income sources. This is common enough really - you might have a rental house from which you derive some landlord income, you might have a side business, you might have a consulting gig from time to time, you might just drive for Uber on the weekends (this doesn’t generally net you much anymore but for a while people used to pull in some spending cash this way if you were in the right city). Of course, the Tortuga crowd has traditionally emphasized job stacking - which if you’ve got the energy and agency to do so, can certainly put you ahead on the income bracket for a while, and could let you bootstrap your way into one of the other options like building a real estate portfolio or dividend income or the like. (Really though: if you’re going to do that, you should plan to only do it for a finite period of time and typically for a particular goal like buying your house or building your investment portfolio to a certain target value or clearing your debts or whatever - or perhaps for a certain duration - it’s awfully easy to burn out otherwise if you make it your lifestyle for a long time frame.)

Or, hell, a business built on vending machines or a laundromat, who am I to judge? I know people who have made a solid income stream out of both of those - not my cup of tea, but they seem to find it workable, and as I’ve been told endlessly: “beats hanging drywall!” (yeah, I bet!)

There’s also a section on how to maximize the multiple-income-stream lifestyle paired with the stay-at-home spouse for those of you looking to do the trad homemaker sort of life. It may be aspirational - it may be a good thing to plan to “move into” as you start to build a family - the concept of being an “Etsy mom” instead of a part time RN or substitute teacher is perhaps attractive to some, but the thought of also just focusing on running the family and the household (or maybe the volunteer and charity efforts, depending on your inclinations and income level) is probably something that appeals to many.

And - at special request - I’m taking a look at how a couple of high profile people managed to use the Traditional IRA and Roth IRA systems to each grow an absolutely huge tax free savings: Mitt Romney and Peter Thiel.

So… when you start complicating things with multiple streams of income… what’s different?

Tax planning becomes more complex with multiple income sources because your total combined income determines your overall tax bracket, potential underwithholding or overwithholding, and eligibility for certain deductions or credits. The IRS treats all income as part of your adjusted gross income (AGI), but each type has unique rules for reporting, taxation, deductions, and payments. Under current 2026 laws (including permanent extensions from the 2017 TCJA and the One Big Beautiful Bill Act, or BBB), key brackets are progressive (10% to 37%), with the top rate kicking in over $626,350 for single filers or $751,600 for married filing jointly. Long-term capital gains rates are 0%, 15%, or 20% based on income thresholds. Standard deductions are $15,750 (single), $31,500 (married filing jointly), or $23,625 (head of household). State taxes may (usually do) add layers, but this focuses on federal tax implications. Use this document as a baseline and also consult with a tax professional - especially if you have to deal with state taxes.

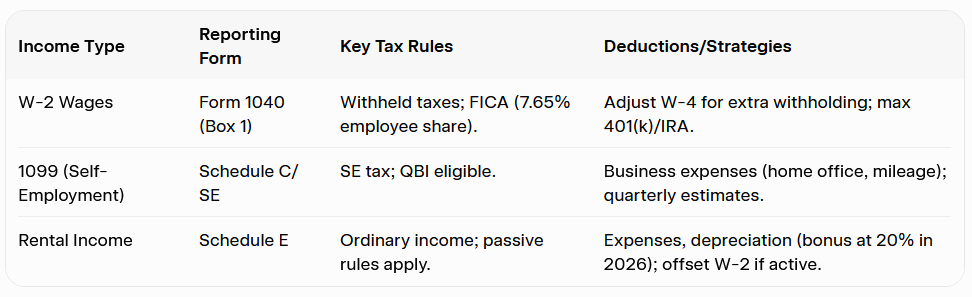

You’ll report everything on Form 1040, attaching schedules as needed (e.g., Schedule C for 1099 business income, Schedule E for rentals). Common pitfalls include underpaying estimated taxes (leading to penalties) or missing deductions. Strategies like adjusting Form W-4 withholdings, making quarterly payments, and maximizing retirement contributions can help. Use the IRS Tax Withholding Estimator for personalization.

There are some key tax planning differences with multiple income sources. The sort of obvious one involves combined income pushing you up into another tax bracket, because income from all sources adds up, which often kicks you into a higher bracket where more of your earnings are taxed at elevated rates (e.g., from 22% to 24%). Cold consolation that only the portion above the threshold is taxed higher. (This is easy to fall prey to if you’re running pass-through entities like S-corps or LLCs with S-elections - a recent Tortuga all-hands call had Theon Ultima lamenting exactly that “problem”.) Next major one is going to be withholding vs estimated payments: W-2 jobs automatically withhold taxes, but this assumes it’s your only income - so, multiple sources often lead to underwithholding since there’s an assumption of default deduction. Non-W-2 income (e.g., 1099 or rentals) requires you to handle payments yourself via quarterly estimates (due April 15, June 15, Sept. 15, Jan. 15 - do not miss these dates, the IRS is unfriendly about this) to cover at least 90% of your liability or 100%-110% of last year’s tax (higher if AGI >$150,000). And don’t forget self-employment tax: which applies to 1099 income (15.3% on net earnings: 12.4% Social Security up to $176,100 wage base, 2.9% Medicare unlimited, plus 0.9% additional Medicare on earnings over $200,000 single/$250,000 joint). Deduct half as an above-the-line adjustment. You’ll definitely want to watch for deductions and offsets: business expenses (Schedule C), rental costs/depreciation (Schedule E), and losses can reduce taxable income. Passive activity rules limit rental losses to passive income unless you qualify as a real estate professional (750+ hours in real estate, which is not actually all that crazy hard to qualify for). Up to $25,000 in rental losses can offset other income if AGI <$150,000 and you actively participate. Beware of the “edge case” additional taxes like Net Investment Income Tax (NIIT, 3.8%) on rentals/investments if your modified AGI >$200,000 single/$250,000 joint - also, there’s additional Medicare tax on high wages/self-employment (and annoyingly, you really don’t get anything in return for that, other than the privilege of helping keep Medicare going).

Let’s also look at the important optimization strategies, which may not surprise you but certainly bear a look to make sure you can take advantage of them if you can. Certainly contribute to retirement (e.g., traditional 401(k) up to $24,500, or SEP-IRA for self-employed up to $70,000 total) to lower AGI. Use HSAs (up to $4,150 single/$8,300 family) for tax-free medical savings. Bunch deductions (e.g., charitable giving) to itemize over the standard deduction. Harvest capital losses to offset gains (and also up to $3,000 per year against ordinary income, which can roll over if you have a lot of losses). Consider QBI deduction (20% on qualified 1099/pass-through income, subject to limits).

The common categories you’ll (tend to) hit:

OK - first requested scenario. Let’s say you have a standard W-2 (paycheck) job - and also landlord income. This is a pretty common thing, which will still cause you heartburn come tax season if you don’t do it right (but also, it’s pretty easy to get it right - because it tends to be pretty predictable!) Just plan for it ahead of time.

Rental income is taxed as ordinary income, added to your W-2 wages, and follows the same brackets. It’s generally passive, so losses are limited to other passive income (carry forward excess), but if you materially participate and AGI <$100,000-$150,000 (phaseout), up to $25,000 can offset W-2 income. There’s no self-employment tax on pure rentals, but NIIT may apply.

As far as planning ahead for this: Track all your expenses (repairs, insurance, property taxes—SALT cap $40,000 under BBB) - a Google Sheet or Excel document is fine, hell, you can just keep all the receipts in a shoebox and give them to your accountant if you don’t mind paying them to unwind it all, but it’s a little silly because this is easy enough to classify yourself. Use depreciation (e.g., 27.5 years for residential) or bonus depreciation for improvements. If short-term (e.g., Airbnb average less than 8 days), it may qualify as active business income, allowing losses to offset W-2 and QBI deduction. Adjust W-4 to withhold more from paycheck for rental income, or pay estimates. Convert to/from personal use carefully—special proration rules apply.

Second requested scenario - for people moonlighting, especially for the Tortuga crowd - honestly, I should have written this the moment I walked in the door there, because several people I have talked to here seem to be getting spanked by the IRS courtesy of holding multiple jobs - but this section is specifically if you have both a conventional W-2 job and 1099 income. Classically this was a paycheck job and a side moonlighting “consulting” gig for a few extra hours or some expert witness work or something (or something you do during the summer while school’s not in session) - these days it can be more aggressive job stacking, some people are holding down several jobs at once and … damn, do you guys ever sleep? Anyway, it’s applicable with multiple 1099s as well.

This mix combines withheld W-2 taxes with self-managed 1099 obligations. Your total income sets brackets, and 1099 adds SE tax, but you get deductions W-2 workers don’t.

My basic tips: Report 1099 on Schedule C; deduct expenses (e.g., supplies, 50% meals through 2025). Claim QBI (20%) if eligible - there’s no phaseouts for most below $182,100 if filing single/$364,200 joint. Use W-4 Step 4(c) to withhold extra from W-2 for SE tax, or pay quarterly (which is essential to avoid penalties, you’re probably going to need to watch for this and make sure you adjust if your earnings are sort of uneven). If your 1099 job is a side gig, track mileage (67 cents/mile in 2026) and home office expenses. Self-employed health insurance is 100% deductible - and that can be a sizable chunk of change these days. Solo 401(k) or SEP-IRA can shelter more than a standard 401(k) - I’ve talked elsewhere about how to use these for disproportionate benefit.

The extremely related (third) scenario for the Tortuga crowd - or even just the classically overworked sort - is when you have two or three jobs - and thus have multiple W-2s.

All W-2 income is combined on Form 1040; each employer withholds independently, often leading to underwithholding since they don’t “see” your other jobs - if you work “evenly” for these other jobs, this will nearly always happen. This can bump you into higher brackets or trigger additional Medicare tax.

As far as planning for this: use W-4 Step 2 checkbox for multiple jobs - it applies higher withholding rates. Or add extra in Step 4(c). If over $176,100 total wages, claim excess Social Security withheld as a credit. No SE tax, but monitor for NIIT if investments involved. Bunch 401(k) contributions across jobs (total limit $24,500).

In all cases, consult a tax pro if your income is over $100,000 - (if you’re successfully job stacking knowledge worker jobs this may be pretty easy) or complex (e.g., multi-state - pretty common for the remote worker). Early planning avoids surprises… start with last year’s return as a baseline, but also if you know that things are going to be a hairball, start before tax season causes everyone to become short on time and patience.

Now, you’re in a little bit different of a situation if the alternate income stream you’re talking about is a pension from your first job (and you’re supplementing it in your second career) - it’s kind of a nice problem to have, mind you, but it’s a bit rare these days. Still, people started poking me about it (it often seems to be the case if you had a government job for a while and retired but still want to work, if so - more power to you). So let’s talk about that, too.

Tax planning for a salary (W-2 income) combined with pension income involves treating both as ordinary income that aggregates to determine your overall tax bracket and liability. Pensions are generally taxable (fully or partially, depending on any after-tax contributions), reported on Form 1099-R, and added to your W-2 wages on Form 1040. This can push you into higher brackets, increase the taxability of Social Security benefits if you’re receiving them, and require proactive withholding adjustments to avoid penalties. Under 2026 rules, including inflation adjustments and provisions from the Big Beautiful Bill (I will never be able to say this with a straight face), key thresholds like standard deductions and a new senior deduction may help offset some impact.

There are some key tax planning differences. Combined income and brackets is of course a major one: both salary and the taxable portion of your pension count as ordinary income, summed for AGI. This total determines your bracket (e.g., 10%-37%), with only the excess over each threshold taxed at the higher rate. For example, if your salary is $60,000 and pension adds $30,000 taxable, your $90,000 total might shift from the 12% to 22% bracket (threshold ~$47,150 single in 2026).

Taxation of pension is going to be one to put careful eyes on. It’s fully taxable if employer-funded with no after-tax contributions; partially nontaxable if you have a cost basis (recover via Simplified Method for most qualified plans - divide basis by expected payments based on age/life expectancy tables). No self-employment tax applies, unlike 1099 income.

Withholding and payments - salary has automatic withholding via W-4, but pensions use optional withholding on Form W-4P (treated like wages unless you elect none). If underwithheld across sources (e.g., owing >$1,000 or <90% of liability), pay quarterly estimates to avoid penalties - pretty much like anything else with the IRS.

As far as additional taxes, high combined income (> $200,000 single/$250,000 joint) may trigger 0.9% additional Medicare tax on wages/pensions or 3.8% NIIT on nonqualified pensions. Also, there’s potential social security impact: if you are receiving social security disbursements alongside, pensions increase “provisional income” (AGI + nontaxable interest + half of social security), potentially taxing up to 85% of benefits if over $25,000 single/$32,000 joint. If that applies to you, there are some senior-specific rules: if you’re 65+ by end of 2025, claim a new BBB-based deduction of up to $6,000 (individual) or $12,000 (joint) above the standard deduction - there’s no itemizing needed, but phases out starting at $75,000 MAGI single/$150,000 joint. Also, standard deduction rises to $16,100 single/$32,200 joint/$24,150 head of household, plus existing extra for 65+ (~$1,950 single/$3,900 joint). RMDs required if 73+ (or 75+ if born 1960+); failure incurs 25% excise tax. (Be careful about that!)

The optimization strategies are going to be similar to what I usually tell you, but there’s some pension-specific material - and I’ll be the first to say there may be other fancy maneuvers beyond what you see here, pensions aren’t my area of expertise, but this should get you in the right ballpark at least. Certainly start by adjusting witholdings: update W-4 for salary to withhold extra, or W-4P for pension to cover the gap - use IRS Tax Withholding Estimator. As ever, retirement contributions are a great way to finesse your tax bill: if still working, max salary deferrals (e.g., 401(k) up to $24,500 + $8,000 catch-up if 50+, or more if 60-63) to lower AGI and offset pension tax. Deductions and credits are always ideal if you can take them: bunch itemized deductions (e.g., SALT up to $40,000 cap under BBB) if exceeding standard; claim senior deduction if eligible. Public safety officers exclude up to $3,000 for health premiums, so you should definitely do that if it applies. And to the extent that you can, there’s going to be some useful things to do with timing and planning. In the broad camp of timing and rollovers, you may want to delay your pension start if possible (yes, I realize this sounds unintuitive, but your payout is likely to be higher if you can do so); rollover lump sums to IRA to defer tax (20% withholding if not direct). For early pensions (<59½), avoid 10% penalty with exceptions like age 55+ separation. And to the extent that you can do multi-year planning for your financial needs - and I realize this isn’t always in the cards, but if you can - forecast RMDs, SS, and salary to stay in lower brackets; consider Roth conversions if your pension is traditional.

If income is high or involves SS/RMDs, consult a tax advisor… rules can vary by pension type (qualified vs. nonqualified).

But for Tortugans in particular - and other folks who might have occasion to draw multiple paychecks at the same time - the employment scenario that will generally frustrate you the most when dealing with the IRS is multiple conventional W-2 jobs, because the system isn’t generally set up to handle it and the assumption is that you haven’t got more than one (so the defaults and withholdings are going to be very much off-base, leaving you having to do a lot of recalculation).

The best ways to mitigate taxes with multiple W-2 jobs focus on two main goals: (1) fixing inaccurate withholding to avoid surprises/penalties, and (2) reducing your actual taxable income through pre-tax accounts and deductions. Multiple employers mean each withholds taxes independently (often assuming you’re their only job - well, it’s ordinarily a pretty safe assumption), which frequently leads to under-withholding overall. You file one Form 1040 combining all W-2s, so total income determines your brackets, but you can still optimize aggressively. Here’s a prioritized list of the most effective, legal strategies (based on 2026 rules):

First, fix your withholding with updated W-4 forms (this is almost certainly going to be your biggest cash-flow fix). Each employer doesn’t know about your other jobs, so you often end up under-withheld and owing money (plus potential underpayment penalties) or over-withheld and giving the IRS that infamous interest-free loan. Use the free IRS Tax Withholding Estimator tool at IRS.gov (enter your paystubs from all jobs). It tells you exactly how to fill out your W-4s. Then, submit a new Form W-4 to each employer. Step 2 (multiple jobs and/or spouse works) - unsurprisingly, use the Multiple Jobs Worksheet, check the box if you have exactly two similar-paying jobs, or add extra withholding (usually on your highest-paying job via Step 4(c)). Check withholding again mid-year or after any pay change. This doesn’t reduce your tax bill - it just prevents surprises and penalties - and the IRS will be happy to hand those out otherwise.

As usual, I’ll give you the recommendation to maximize pre-tax retirement contributions across all jobs. This directly lowers your W-2 taxable wages right away (and builds wealth, which is what you are actually after, as much as we’re sort of in the game of mitigating taxes - this is all actually so you can build your wealth, after all).

There’s the 401(k)/403(b): the 2026 employee deferral limit is $24,500 total across all plans (plus $8,000 catch-up if 50+, or higher $11,250 catch-up if age 60–63). You can split contributions between jobs if needed. Now, there’s a huge advantage of multiple jobs: Employer matches are calculated separately per plan. Max out matches from every employer for free money (not limited by your $24,500). Overall annual additions limit per plan is $72,000 (your deferral + employer match + any after-tax). Also, you may have access to the 457(b) plans (governmental or certain nonprofit jobs): These have a separate $24,500 limit - so this is a perfect double-dip if you have one. If a plan allows after-tax (non-Roth) contributions, consider a “mega backdoor Roth” for even more tax-free growth. Prioritize getting full matches everywhere, then fill your deferral limit.

Max an HSA (if you’re eligible - this is triple tax-advantaged) - if any job offers a high-deductible health plan (HDHP), the 2026 limits are roughly $4,400–$4,450 self-only or $8,750–$8,950 family (+$1,000 catch-up if 55+). Contributions are pre-tax (or deductible), growth is tax-free, and qualified medical withdrawals are tax-free. It’s probably the best “hack” available to W-2 employees. You usually can’t pair this with an FSA on the same plan.

There are some other quick wins to look for if you can. FSA (Flexible Spending Account) lets you use pre-tax dollars for medical or dependent-care expenses if offered by any employer (use-it-or-lose-it rules apply). Social Security over-withholding: If your combined wages exceed the 2026 wage base (~$184,500), the excess Social Security tax withheld gets refunded automatically on your return. Itemized deductions or credits: Bunch charitable donations (or use a donor-advised fund), mortgage interest, etc., if they beat the standard deduction. Claim all available credits (child tax credit, education credits, etc.). Above-the-line deductions: Student loan interest, etc.

Less quick but still very useful… let’s call them advanced options (for higher combined income) would include topics that you have probably already heard me talk about, but I’m going to mention again because you should certainly consider all three of these: tax-loss harvesting in brokerage accounts, real estate strategies (e.g., short-term rentals with cost segregation or having a spouse qualify as a “real estate professional” to generate passive losses that offset W-2 wages), and you should almost assuredly look to do backdoor Roth IRA contributions. All of these can create bigger reductions but often need a CPA or tax attorney.

As a general rule, you probably want to start with the IRS Withholding Estimator + new W-4s today, then max every pre-tax account available (401(k) deferrals, matches, HSA). This combo usually saves the most money and hassle for people with multiple W-2s. Run the numbers mid-year, and strongly consider a tax professional or good software - especially with recent tax law changes (like the Big Beautiful Bill impacts) and/or if your total income is high. State taxes, local rules, and your exact situation can vary. This is general information, and will generally also benefit from some personalized advice - especially because state tax situations and pension intricacies may be complicating (and you will probably want to be able to make and work against a multi-year plan… at least as much as you can, what with the likelihood of legislators jacking around the tax code again).

The other thing that will frequently throw you off is realized investment gains. If you trade the stock market - I suppose I should say if you successfully trade the stock market, and most particularly if you do so on a short-term-capital-gains basis, you tend to generate income that wildly distorts your tax results for the year. While I will be the first to say this this is a nice problem to have, (hey! you made money! don’t complain!) it can still leave you at very least wincing when April rolls around and you have to write out a big check to the IRS (one hopes you have done proper withholding before then). It is difficult to give any one particular recommendation on this front, but you can certainly engage in tax loss harvesting (selling losses to counterbalance gains) and you can often to a certain extent be judicious about when you book your gains so as to push those into a next quarter or next year - but that’s of course not always possible, the market may not wait for you. It may be feasible for you to hedge a particular stock price (if you think it won’t hold) - a collared transaction can be used specifically to give you time to divest at a certain price point and effectively remove volatility from a stock that otherwise might heavily oscillate; famously, Mark Cuban wisely put an enormous stock collar on his Yahoo shares after selling Broadcast.com and was able to retain billions of value even when Yahoo stock … didn’t retain that value.

Some hopeful Tortugans asked me to comment on the value of job stacking when combined with marriage - so that your wife can focus on being a homemaker (raising the kids, and otherwise being trad). Sure, ok - it’s … actually, pretty much right there in black-and-white: deductions are higher if you’re married; there are additional child credits, and you can also fund your spouse’s IRA contributions.

Married filing jointly (MFJ) is almost always the best status here. It creates a “marriage bonus” for single-income households because deductions, brackets, and many credit limits are roughly doubled without doubling your taxable income.

There is a much higher standard deduction. In 2025: $31,500 for MFJ (vs. $15,750 if single). For 2026, $32,200 for MFJ. This alone can wipe out a big chunk of one spouse’s earnings from taxes. If you’re 65+ or blind, you get extra amounts on top. There are also wider tax brackets, by which I mean income is taxed at lower rates. MFJ brackets are approximately double those for singles, so more of your household income stays in the lower brackets. 2025 MFJ brackets (taxable income after deductions): 10%: $0 – $23,850, 12%: $23,851 – $96,950, 22%: $96,951 – $206,700, and so on (higher brackets also roughly doubled). A single filer with $100k income would hit the 22% bracket much sooner than a MFJ couple with the same household income. Then, you can also do spousal IRA contributions. The working spouse can fund an IRA (Traditional or Roth) for the stay-at-home spouse up to the full annual limit, using the working spouse’s earned income. The 2025 limit: $7,000 per person ($8,000 if age 50+), the 2026 limit is: $7,500 ($8,600 if 50+). Your total combined contributions can’t exceed the working spouse’s compensation (so you can’t do this all off savings, for instance). This is a huge way to build retirement savings (and potentially take a deduction) for the non-working spouse. You must file jointly to qualify. And of course, since you’re in theory doing this for pronatal reasons: Child Tax Credit (CTC) + other family credits (if you have kids). Up to $2,200 per qualifying child under age 17. Up to ~$1,700 of that can be refundable (Additional Child Tax Credit) if you owe little or no tax. Phase-out starts at $400,000 modified AGI for MFJ (exactly double the single threshold of $200,000). You also get better phase-out ranges for the Earned Income Tax Credit (EITC) and other credits when filing jointly.

Don’t forget, of course, the Health Savings Account (HSA) (if you have a qualifying high-deductible health plan): Family contribution limit is higher (~$8,550 in 2025). Triple tax-free: deductible, growth tax-free, and medical withdrawals tax-free. Great for kids’ medical/dental costs. Orthodontics especially add up - although the Invisalign ones are a lot less brutal (at least to wear, and seemingly a little less harsh on the pocketbook) than braces used to be!

Itemized deductions are generally a winner - well, only if they exceed the $31,500 standard deduction - but it does seem like this is not hard to do these days. The one that usually gets you there-or-close is mortgage interest on your home. Also, state & local taxes (SALT) - cap temporarily raised to $40,000 for MFJ in 2025 in some updates. Don’t overlook charitable donations (cash or goods). And you never want to face these, but to the extent that you have them (they do come up) you can deduct unreimbursed medical/dental expenses (only the amount over 7.5% of AGI).

In the annoyingly-similar-name camp we have what are referred to as Above-the-Line Deductions (which reduce AGI even if you take the standard deduction) - so even if you’re not itemizing deductions, these are worth paying attention to… effectively they’re “the even more generally applicable version” of the same thing: Student loan interest (up to $2,500), Traditional IRA/spousal IRA contributions, HSA contributions, Self-employed health insurance deduction (if applicable).

There’s some education-related benefits - (when kids reach college age or if you’re retraining or otherwise taking classes) - American Opportunity Credit (up to $2,500) or Lifetime Learning Credit. Also the 529 plan contributions (growth is tax-free; many states offer extra deductions).

Then there’s some other sort of family-friendly ones that I am going to mention which may be applicable to you. There’s still a bunch of energy-efficient home improvements, solar, or EV credits (some at a state level, some at a federal level). If self-employed or you have a family business: Deduct legitimate business expenses; pay kids under 18 (wages often payroll-tax-free and deductible for you). Child & Dependent Care Credit or Dependent Care FSA - though this is limited if one parent stays home full-time with no work-related care expenses - but if for instance one parent is full time and the other has part time work, you may get a lot of mileage out of it.

Pro tip: max out your pre-tax accounts (401(k), IRA, HSA) first … this lowers your AGI and can help you qualify for more credits or avoid phase-outs. Bunch charitable donations or medical expenses into one year if you’re close to itemizing.Marriage with a stay-at-home spouse and kids usually saves thousands compared to filing single (or even married filing separately). The exact savings depend heavily on your income, number of kids, state of residence, and whether you own a home or have high medical/education costs. Use free IRS tools, TurboTax/H&R Block estimators, or see a tax professional for a precise calculation - especially since rules can have certain sticky points (e.g., qualifying child tests, MAGI calculations). Check IRS Publication 501 or the instructions for Form 1040 for full details.

And then for those of you who have been reading through this article patiently with daydreams of moonshot tax-free growth, yes, you’ve made it to the guide to being Peter Thiel or Mitt Romney:

Let me start with the quick disclaimer - you’re probably not going to be able to replicate either of these. Not because you can’t do the basic maneuver that Thiel did, which is “put a big chunk of founding stock into your Roth IRA” - but because it requires you to then found Paypal and take it through to IPO, and then follow that on by investing in early stage Facebook and see it through to one of the world’s most valuable companies. Friends, if you can do those, the key part is not the Roth IRA - you’d be a billionaire either way! (It’s also nice, sure.)

Peter Thiel leveraged explosive growth in a Roth IRA by using it to hold massive stakes in high-potential, early-stage private companies - primarily his own startup, PayPal, and then later investments like Facebook - where the shares were acquired at extremely low valuations inside the tax-advantaged account. All subsequent appreciation and gains grew tax-free (and remain tax-free on qualified withdrawals after age 59½), turning a small initial contribution into billions without ever paying capital gains taxes on the windfall.

Based on ProPublica’s 2021 investigation (and the IRS guidelines), here’s the key steps on how he did it.

In 1999, Thiel opened a Roth IRA and contributed around $1,700–$2,000 (within the annual limits at the time; his income that year was about $73,000, qualifying him).

He used a self-directed Roth IRA (which allows alternative investments like private company stock, unlike standard brokerage IRAs limited to public securities).

Then, during PayPal’s formation (then called Confinity) - or maybe during early merger phase, I’m not actually clear, Thiel purchased 1.7 million shares through the Roth IRA at a par/founders’ price of just $0.001 per share (a tenth of a penny).

Total cost inside the IRA: $1,700.

This gave the Roth IRA a huge ownership stake in the company right from the start.

Sounds easy enough - he started small, he risked basically a year of his Roth savings (by buying highly illiquid founding shares of Paypal) - and it paid off big.

Well, it turned out that PayPal grew rapidly. When eBay acquired it in 2002 for $1.5 billion, Thiel’s shares (held in the Roth) were worth about $55.5 million—a massive multiplier.

Because the shares were inside the Roth IRA, none of that ~3,200x+ gain was taxed as capital gains. The entire value stayed sheltered.

That’s an excellent start. But what really made Peter Thiel’s name was basically doing this again - from an angel investor / venture capital perspective. You see, Thiel rolled the proceeds into other high-growth private investments. A notable one was an early stake in Facebook (reportedly around $500,000 invested via the Roth).

As Facebook (and other ventures) skyrocketed, the account continued compounding without taxes dragging down returns.

By the end of 2019, the Roth IRA reached $5 billion (up from under $2,000 in 1999), with jumps like $3 billion+ in just a few years from private equity-style gains.

He reportedly made no further contributions after 1999 - basically all growth came from internal investments and appreciation. The power of reinvesting and compounding tax-free is pretty phenomenal, especially when you got in on Facebook, Yelp, SpaceX, Spotify, Palantir, and AirBNB (let’s be fair though - a very disproportionate amount of those gains are from his early investment in Facebook stock).

So, why did this work so well? Well … apart from the outrageous luck factor of hitting the startup lottery twice in a row with Paypal and then Facebook, which is not to be overlooked … there’s some important planning factors here. The first major leverage point is of course the Roth IRA rules: contributions are after-tax, but qualified growth and withdrawals are 100% tax-free - no capital gains, dividends, or distributions taxed if rules followed. Furthermore, doing this in a Roth self-directed structure allowed buying illiquid, pre-IPO/private shares unavailable in regular IRAs.

Combine this with the exceedingly favorable share price available to him: as a founder (well, co-founder), Thiel could buy huge blocks of shares at rock-bottom founders’ prices or valuations that public investors couldn’t access; similarly, when it came time for him to invest in Facebook, the price point he was able to buy in at was far more attractive than what future investors would be able to participate at.

Now, in a taxable account, he’d have paid long-term capital gains (15–20%+) on sales or realizations; in the Roth, zero tax on the billions in appreciation. The lack of tax drag on compounding has been tremendously advantageous over the years. ProPublica dubbed it “Lord of the Roths” and highlighted how this turned a middle-class savings tool into a ultra-wealthy tax shelter, leading to complaints about how this was costing the government potentially billions in lost revenue (which seems like “you did what you were supposed to do but you did it too well!”) by following these rules. I haven’t heard if the proposed wealth taxes target IRAs that are too big, but I suppose I wouldn’t be surprised.

Important caveats (aka, You Probably Can’t Replicate This Exactly) - as noted, this strategy relied on being an insider at hyper-successful startups (first PayPal and then the eBay exit; followed by the even more spectacular return on an early investment in Facebook). Average investors, to put it mildly, lack access to founders’ shares at $0.001 or equivalent.

Self-directed IRAs can hold private stock, but:

Valuations must be arm’s-length/fair market (there’s significant IRS scrutiny on self-dealing).

Prohibited transactions (e.g., self-dealing with disqualified persons) can disqualify the IRA.

Annual contribution limits still apply (~$7,000 in 2025/2026, plus catch-up), so scale comes from growth, not big deposits.

Thiel’s case sparked debate about Roth IRA “abuse” and calls for reforms (e.g., limiting mega-IRAs), but as of 2026, the core mechanics remain legal for those with the right opportunities.In short: Thiel didn’t “hack” the system illegally… he maximally exploited the Roth’s tax-free compounding by loading it with asymmetric, high-upside private equity bets that exploded in value. It’s a masterclass in placing your highest-conviction, highest-growth assets inside the most tax-efficient wrapper possible.

If you’re planning to try to do this: the “disqualified persons” bit is going to potentially be a bugaboo.

A disqualified person for a Roth IRA (or actually any IRA) is an individual or entity closely related to the account owner - such as a spouse, lineal descendant (child/grandchild), ascendant (parent/grandparent), or their spouses - who is prohibited from engaging in transactions with the IRA to prevent self-dealing. Prohibited transactions include buying, selling, or leasing property, or receiving personal benefits from IRA assets. So, for instance, investing in your own company is generally not permitted. OK wise guy, so wait… then how did Thiel do it? Well, for entities, the IRS guidelines are: a corporation, partnership, trust, or estate in which the IRA owner has a 50% or greater interest; for Confinity (nee Paypal) our case study Peter Thiel had a couple partners (Max Levchin and Luke Nosek) - and thus Thiel had an only a minority interest of the company to put into his IRA. But still a very significant chunk, as it turned out.

To be fair… you’re probably not going to be able to replicate Mitt Romney’s strategy either, because you’re probably not going to be in a lead position at a powerful private equity firm. But it’s still instructive to know.

Mitt Romney grew a substantial portion of his wealth in a tax-advantaged retirement account… specifically, a large traditional IRA (not a Roth IRA)… through aggressive use of private equity investments during his time at Bain Capital. Unlike Peter Thiel’s Roth IRA (which allows completely tax-free growth and withdrawals), Romney’s was a pre-tax (traditional) IRA, meaning contributions were tax-deductible, growth was tax-deferred, and withdrawals are taxed as ordinary income. However, the massive appreciation inside the account effectively sheltered enormous gains from immediate taxation, allowing the wealth to compound without annual capital gains taxes.This strategy drew significant attention during his 2012 presidential campaign, when financial disclosures revealed his IRA was valued between $20 million and $102 million (with estimates often cited around $100 million+). More recent analyses (as of the early 2020s) suggest it could be in the range of $25 million to $125 million or even higher, though exact current figures aren’t publicly updated. The key was not exceeding contribution limits illegally but leveraging insider access to high-upside, low-initial-valuation private investments.

As far as the key component of how it worked… well, the one you’re going to have the hardest part with is that Romney co-founded and led Bain Capital from 1984 to 1999 (with some involvement extending later). Bain allowed certain partners and employees (including Romney) to co-invest in the firm’s deals via their retirement accounts, often using a SEP-IRA (Simplified Employee Pension IRA, which permitted higher annual contributions - up to around $30,000 per year during that era - funded by the employer).

So critically, this gave him (and others) access to extremely low-valuation stakes in private deals. This was a pretty sweetheart arrangement. Bain structured investments with multiple share classes. Employees could use their IRAs to buy “Class A” or similar preferred shares (or partnership interests) at very low valuations - sometimes nominal, almost near-zero - because they represented high-risk, future-oriented upside (e.g., carried interest-like profits or profits interests in portfolio companies).

These were often valued using methods like “liquidation value” or future income projections, which experts noted could be significantly below what later proved to be fair market value. When Bain’s deals succeeded (e.g., leveraged buyouts that generated massive returns), these stakes exploded in value inside the IRA.

Naturally, being an IRA, this resulted in tax-free compounding. No capital gains taxes were due on the appreciation while inside the IRA. The entire growth compounded tax-deferred until withdrawal (now required via Required Minimum Distributions since Romney is over age 73). There was also no contribution limit bypass needed -annual limits were followed, but there is no cap on how much an IRA can grow internally through investments. A small initial amount (or modest annual max contributions) could balloon if the underlying assets multiplied dramatically (just as we saw for Thiel).

I should also mention offshore and blocker structures: some Bain funds used offshore entities (e.g., in the Caymans) to help retirement accounts avoid unrelated business income tax (UBIT) that might otherwise apply to leveraged investments - though Romney has stated this provided him no personal tax reduction. It likely wouldn’t have mattered for him, given that this was in his IRA.

By comparison to Peter Thiel’s approach: Thiel used a Roth IRA for similar private equity bets (e.g., ultra-cheap PayPal founders’ shares), achieving true tax-free status on billions in growth. Romney’s traditional IRA deferred taxes but doesn’t eliminate them - distributions are taxed at ordinary income rates (up to ~37%). If Romney had used or converted to a Roth, the wealth would have been even more tax-efficient. (If you’re asking “Why didn’t he? Surely Romney was smart enough and well-advised enough by tax professionals” the answer is that the Roth wasn’t introduced until 1998.) His setup was still extraordinarily advantageous for someone with access to elite private deals unavailable to most investors.

Why this isn’t replicable for most people? Well, pretty sure you know that answer if you’ve read this far. It requires you to be an insider - heck, basically a founding insider - at a top private equity firm to access those low-valuation opportunities. Bain Capital was absolutely top shelf. Further, self-directed IRAs can hold private equity today, but valuations must be arm’s-length and fair market (IRS scrutiny on self-dealing is high). And prohibited transaction rules prevent conflicts (e.g., you can’t invest in your own company in ways that benefit you personally).

Again, this sparked debates and GAO reports on “mega-IRAs,” leading to calls for reforms (e.g., balance caps), but the core rules allowing unlimited internal growth remain.

In essence, Romney maximized tax-deferred compounding by placing asymmetric, high-growth private investments inside his IRA - legal, eyebrow-raising, but reliant on his position at Bain. It’s a prime example of how retirement accounts can become powerful wealth-building tools for those with exceptional investment access, though his wasn’t fully “tax-free” like a Roth. For personalized strategies, consult a tax professional, as rules evolve. Though to be fair, if you’re in a position to pull this off - you probably have already worked it out with your tax professional.

All of that being said… if you are actually going to try and replicate Thiel’s maneuver, you need several co-founders (like Paypal had) - you can’t do this if you own too big a piece of the firm yourself (or with your spouse or your family). I will say - it’s not a bad idea to do it (but I have never done it, or perhaps I should say, I have not yet done it; yes, I have worked out a good blueprint - if I get enough interest, I’ll do an article on how to do that for paid subscribers - or you can ask me about it in Tortuga chat). Romney’s is … easier to do, but it still requires a position of exceptional privilege from which to cleverly stuff your IRA (or potentially Roth IRA) with very strategically undervalued assets. I suspect you could probably do this pretty readily if you didn’t mind the appearance of grift, or if you were in Congress with certain access to privileged information (eg the famous Pelosi Stock Trading record) - but I should advise you against making decisions that will get the IRS or the SEC after you. You want to be able to enjoy your prosperity happily, after all.

| A guest post by

|